TL;DR:

- A cash-out refinance replaces your existing mortgage with a larger loan, providing cash at closing by tapping into property equity. It involves strict eligibility, LTV limits, and potential rate resets that impact total interest and cash flow, especially for investment properties. Careful analysis of net proceeds, repayment capacity, and alternative options ensures the transaction aligns with real investment goals.

A cash-out refinance is defined as a mortgage transaction that replaces your existing loan with a larger one, paying you the difference in cash at closing. For real estate investors and equity-rich homeowners, this mechanism converts locked-up property value into deployable capital without selling the asset. The cash-out refinance process is governed by loan-to-value limits, appraisal requirements, and closing costs that directly affect how much you actually walk away with. Understanding these mechanics before you apply determines whether the transaction creates real financial leverage or simply shifts debt around.

How does a cash-out refinance work step by step?

The cash-out refinance process follows a defined sequence, and knowing each stage prevents costly surprises. Here is how it moves from application to funded cash:

- Calculate your available equity. Lenders cap the new loan at roughly 80% loan-to-value for conventional loans on most properties. On a $400,000 property, the maximum new loan is approximately $320,000. If you owe $200,000, your gross cash-out potential is $120,000 before fees.

- Submit your application and documentation. Lenders require income verification, tax returns, current mortgage statements, and property details. Investment property applications also require rent rolls or lease agreements.

- Order and complete the appraisal. The appraisal sets the official property value that determines your LTV calculation. A lower-than-expected appraisal directly reduces the cash you receive, so condition and comparable sales matter.

- Underwriting review and loan approval. The lender verifies all documentation, confirms the LTV, and issues a conditional or final approval. Investment properties face stricter scrutiny at this stage.

- Closing and fund disbursement. You sign the new loan documents, the old mortgage is paid off, and closing costs typically range from 2% to 6% of the new loan amount. For a $300,000 refinance, that is $6,000 to $18,000 in fees. The net cash you receive is the new loan amount minus the old payoff and all closing costs. The full timeline from application to cash runs 30 to 60 days, with a federally required 3-day rescission period for primary residences.

Pro Tip: Calculate net proceeds before you commit. Subtract the old mortgage balance and all closing costs from the new loan amount. Many investors overestimate cash-out by $10,000 to $20,000 by ignoring prorated fees and prepaid items.

Investment properties also carry seasoning requirements. Most conventional lenders require you to have owned the property for at least six months before a cash-out refinance is permitted. Some programs extend that to 12 months.

What are the eligibility criteria and LTV limits for investors?

Eligibility for a cash-out refinance differs significantly between residential and investment property scenarios. Investors face tighter constraints at every level.

Core eligibility factors include:

- LTV limits. Conventional loans cap cash-out refinances at 80% LTV for most properties, while investment and rental properties are typically capped at 70% to 75% LTV. This reflects the higher default risk lenders assign to non-owner-occupied assets.

- Credit score minimums. Most conventional lenders require a minimum 620 credit score for cash-out refinances, with better pricing above 740. Investment property loans often require 680 or higher.

- Debt-to-income ratio. Lenders generally require a DTI at or below 43% to 45%. For investors with multiple financed properties, this calculation becomes complex quickly.

- Seasoning requirements. As noted above, most lenders require 6 to 12 months of ownership before a cash-out refinance is allowed on investment property.

- Rental income documentation. Investment property underwriting requires demonstrated rental income coverage and larger equity cushions than primary residence loans.

The table below compares key parameters across property types:

| Parameter | Primary Residence | Investment Property |

|---|---|---|

| Maximum LTV | 80% | 70%–75% |

| Minimum credit score | 620 | 680+ |

| Seasoning requirement | None (most programs) | 6–12 months |

| Income documentation | Personal income | Rental income + personal |

| Closing cost range | 2%–6% of loan | 2%–6% of loan |

The equity calculation is straightforward but often misread. Your maximum cash-out equals the new loan amount at the LTV cap, minus your current mortgage payoff, minus all closing costs. On a $500,000 investment property at 70% LTV, the max new loan is $350,000. If you owe $250,000 and closing costs total $12,000, your net cash is $88,000, not $100,000.

What are the advantages and risks of cash-out refinancing?

A cash-out refinance carries genuine advantages for investors who model the transaction correctly, and real risks for those who do not.

Key benefits include:

- Lower cost of capital. Mortgage rates are consistently lower than unsecured credit lines, personal loans, or hard money. Accessing $100,000 through a cash-out refinance costs far less in interest than the same amount on a business credit card.

- Unrestricted use of proceeds. Cash-out proceeds carry no lender restrictions on how they are spent once disbursed. Investors use them for down payments on new acquisitions, value-add renovations, debt consolidation, or operating reserves.

- Single payment structure. A cash-out refinance replaces your first mortgage rather than adding a second lien. This simplifies debt service compared to carrying a home equity loan or HELOC alongside your existing mortgage.

- Tax treatment. Cash-out proceeds are loan advances, not taxable income. No 1099 is issued, and the funds do not affect your gross income for the year received. Interest deductibility depends on use, per IRS Publication 936.

Pro Tip: If you are using cash-out proceeds to fund a rental property acquisition or renovation, consult a CPA about interest deductibility. Business-purpose use on investment property often qualifies for full deduction.

The risks are equally concrete:

- Rate reset. A cash-out refinance resets your entire mortgage to the new loan’s rate and amortization schedule. If your current rate is 3.5% and the new rate is 6.5%, you are paying a higher rate on the full balance, not just the cash-out portion. This can increase total interest costs by tens of thousands of dollars over the loan term.

- Higher monthly payment. A larger loan balance at a higher rate means a larger required payment. If rental income does not cover the new debt service, the property becomes cash-flow negative.

- Closing costs reduce net proceeds. Fees of 2% to 6% are real costs. Rolling them into the loan increases the balance and the interest you pay over time.

- Foreclosure exposure. Increasing your mortgage balance raises the stakes if income drops or the property sits vacant. This is not a theoretical risk on investment property.

“Choosing a cash-out refinance depends more on whether the new overall payment and closing costs make financial sense than on the headline cash-out amount or rate.” — Mortgage Reports

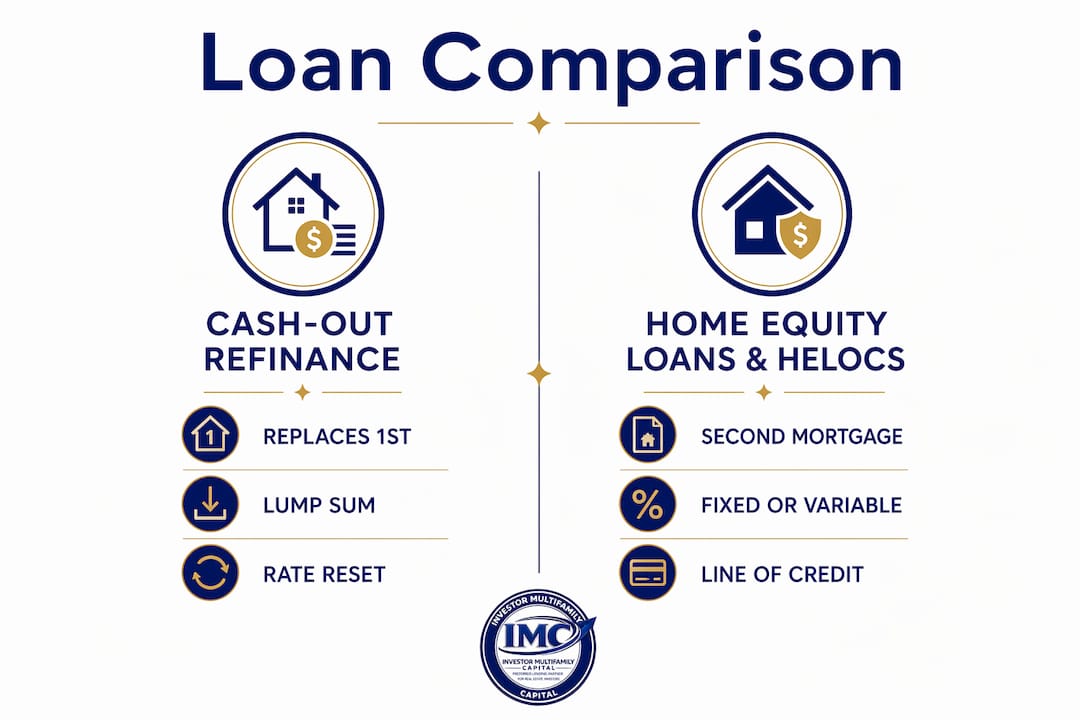

How does a cash-out refinance compare to home equity loans and HELOCs?

Investors accessing equity have three primary tools: cash-out refinance, home equity loan, and HELOC. Each has a distinct structure and cost profile.

A home equity loan is a second mortgage with a fixed rate and fixed payment, layered on top of your existing first mortgage. You receive a lump sum and repay it on a separate schedule. Your first mortgage rate and terms stay unchanged. This is the right tool when you want to preserve a low first mortgage rate and need a defined lump sum.

A HELOC (home equity line of credit) is a revolving credit line secured by your property, typically with a variable rate. You draw and repay as needed during the draw period, usually 10 years. HELOCs offer flexibility for ongoing renovation projects or capital needs that arrive in phases. The variable rate introduces payment uncertainty, which matters on investment property.

A cash-out refinance replaces the first mortgage entirely, resets the rate and term, and delivers a lump sum at closing. It makes the most sense when current rates are near or below your existing rate, or when the cash need is large enough that the cost of a second lien exceeds the cost of refinancing the full balance.

| Feature | Cash-Out Refinance | Home Equity Loan | HELOC |

|---|---|---|---|

| Loan structure | Replaces first mortgage | Second lien, fixed | Second lien, revolving |

| Rate type | Fixed or ARM | Fixed | Variable |

| Fund delivery | Lump sum at closing | Lump sum at closing | Draw as needed |

| Closing costs | 2%–6% of new loan | 2%–5% of loan | Low to none |

| Impact on first mortgage | Replaces it entirely | No change | No change |

| Best use case | Large capital need, rate near current | Preserve low first rate | Phased or ongoing costs |

For investors in New England and Florida markets, the cash-out refinance on rental property is frequently the preferred tool when pulling significant equity for a new acquisition, because it consolidates debt service into a single payment and avoids the subordinate lien complications that arise during a future sale or refinance.

Key takeaways

A cash-out refinance is the most direct way to convert property equity into capital, but the net proceeds, rate reset, and tighter LTV limits on investment properties determine whether the transaction actually pencils out.

| Point | Details |

|---|---|

| Net proceeds calculation | Subtract old mortgage payoff and all closing costs from the new loan amount to find real cash received. |

| LTV caps by property type | Investment properties are capped at 70%–75% LTV versus 80% for most conventional loans. |

| Rate reset risk | Refinancing at a higher rate increases total interest on the full balance, not just the cash-out portion. |

| Tax treatment | Cash-out proceeds are not taxable income; interest deductibility depends on how proceeds are used. |

| Comparison to alternatives | Home equity loans and HELOCs preserve your first mortgage rate but add a second lien and separate payment. |

Why I think most investors get this wrong before they run the numbers

Most investors I work with come in focused on one number: how much cash they can pull out. That is the wrong starting point. The right question is what the new monthly debt service looks like against the property’s rental income, and whether the spread still works after the rate resets.

The rate reset trap is real. If you locked a 3.75% rate in 2021 and you are refinancing into a 7% environment today, you are paying that higher rate on the entire balance, not just the incremental cash. On a $300,000 existing balance, that difference compounds to a significant cost over a 30-year term. Many investors do not model this until after they have already committed.

The second mistake is treating closing costs as a rounding error. On a $400,000 refinance, 4% in fees is $16,000. That is real capital that does not go to work in your next deal. Rolling it into the loan means you are paying interest on those fees for the life of the loan.

Where cash-out refinancing genuinely makes sense for investors: pulling equity from a stabilized asset to fund a value-add acquisition, consolidating high-rate bridge debt after a property seasons, or repositioning capital from a low-yield asset into a higher-return deal. The math works when the new debt service is covered by rental income, the rate differential is manageable, and the deployed capital earns more than it costs.

Work with a lender who underwrites on property cash flow, not just personal income. That distinction matters on investment property, especially when you are scaling a portfolio.

— Joe

Investor MultiFamily Capital cash-out refinance financing

Investor MultiFamily Capital structures cash-out refinance loans specifically for real estate investors in Massachusetts, New Hampshire, Rhode Island, Connecticut, Maine, and Florida. Underwriting is based on property cash flow, not personal income, which means investors with complex tax returns or multiple financed properties qualify on deal merit rather than W-2 documentation.

For investors who want to pair equity extraction with a new acquisition, Investor MultiFamily Capital’s DSCR loan program lets you deploy cash-out proceeds as a down payment and finance the new property on rental income alone. Run your scenario or submit a deal directly to get a same-day review on your cash-out or DSCR deal.

Submit a Deal or Apply Online at investormultifamily.com.

FAQ

What is a cash-out refinance in simple terms?

A cash-out refinance replaces your existing mortgage with a larger loan, and you receive the difference between the two loan amounts as cash at closing, minus closing costs. It converts home equity into usable capital without selling the property.

How much can you cash out on an investment property?

Most lenders cap investment property cash-out refinances at 70% to 75% LTV, which is stricter than the 80% LTV limit on conventional loans. The exact amount depends on the appraised value, your current mortgage balance, and the lender’s program guidelines.

Are cash-out refinance proceeds taxable?

No. Cash-out proceeds are loan advances, not income, so no 1099 is issued and they do not affect your taxable income for the year received. Interest deductibility on the new loan depends on how the proceeds are used, per IRS Publication 936.

How long does a cash-out refinance take?

The process typically runs 30 to 60 days from application to funded cash, including appraisal, underwriting, and closing. Primary residence loans carry a federally required 3-day rescission period after closing before funds are released.

What is the difference between a cash-out refinance and a HELOC?

A cash-out refinance replaces your first mortgage and delivers a lump sum; a HELOC adds a revolving credit line as a second lien without touching your existing mortgage. HELOCs work better for phased or ongoing capital needs, while a cash-out refinance suits large, one-time capital requirements.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.