TL;DR:

- A rent roll is a detailed tenant-by-tenant report that verifies income and assesses risk for lenders.

- A current, accurate rent roll can speed up approval and improve loan terms for multifamily investors.

A rent roll is a tenant-by-tenant report listing each unit, monthly rent, lease start and end dates, occupancy status, and any ancillary income for a rental property. Lenders treat it as the primary document for verifying income sustainability and sizing a loan. For real estate investors seeking multifamily financing or DSCR loans, the rent roll is not a formality. It is the foundation of every underwriting decision. A clean, current rent roll can accelerate approval and improve loan terms. A weak one can reduce your loan size or kill the deal entirely.

What does a rent roll tell lenders?

A rent roll gives lenders a structured view of every income stream tied to a property. It is the first document underwriters reach for when evaluating a loan application, and it answers one core question: is this property’s income real, stable, and sufficient to cover debt service?

A standard rent roll includes the following data fields:

- Unit number and tenant name: Identifies who occupies each unit and confirms the property is not owner-occupied.

- Lease start and end dates: Shows whether leases are long-term, month-to-month, or expiring soon.

- Monthly contract rent: The rent stated in the lease, which may differ from what is actually collected.

- Occupancy status: Flags vacant units, units under notice, and any units held offline for renovation.

- Security deposits: Confirms deposits are held and documents their amounts.

- Concessions: Free rent periods or move-in specials that reduce effective income.

- Ancillary income: Parking fees, pet fees, storage rents, and laundry income that add to gross revenue.

Lenders feed this data directly into net operating income (NOI) calculations and debt service coverage ratio (DSCR) analysis. A DSCR below 1.0 means the property does not generate enough income to cover its loan payments. Lenders typically require a minimum DSCR of 1.20 or higher for standard investment property loans.

Pro Tip: Always separate ancillary income from base rent in your rent roll. Lenders often apply a haircut to ancillary income or exclude it entirely from NOI calculations, so showing it clearly lets you argue for its inclusion.

How do lenders analyze vacancy, WALT, and tenant concentration?

Lenders do not just read a rent roll. They stress-test it against three core metrics: vacancy rate, Weighted Average Lease Term (WALT), and tenant concentration. Each metric signals a different type of income risk.

Vacancy rate thresholds

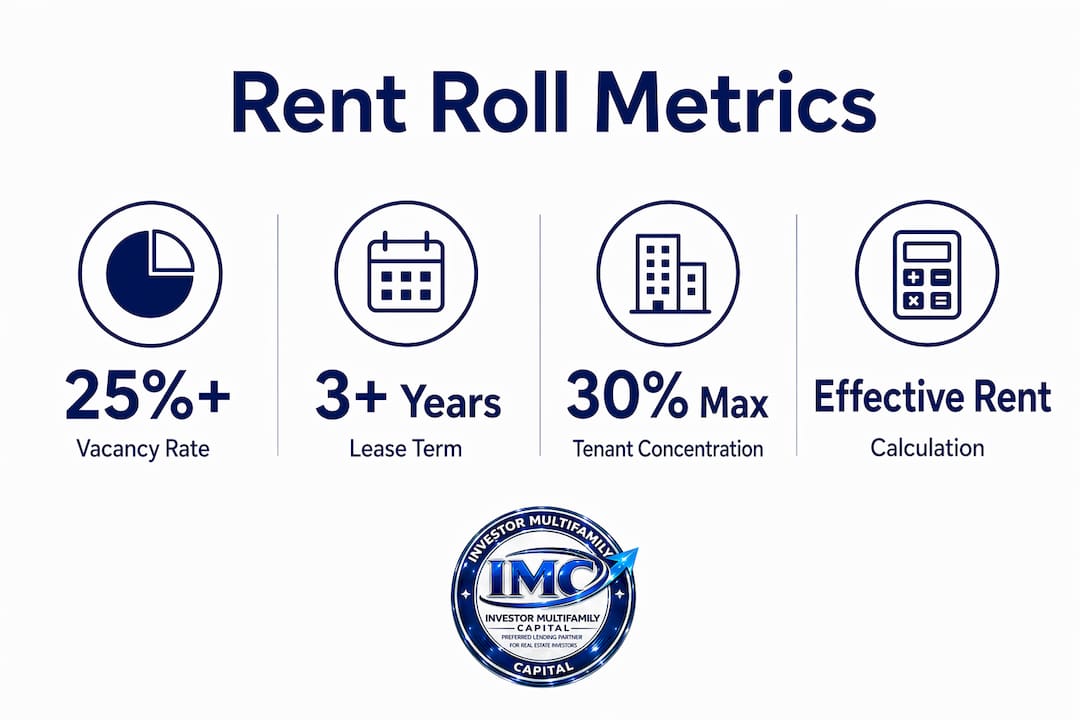

Vacancy above 25% is a red flag that triggers additional scrutiny. That level of vacancy raises questions about the property’s marketability, management quality, and local demand. Institutional lenders typically model a minimum vacancy floor of 5%, even when a property is fully occupied. That floor accounts for normal turnover between tenants.

Weighted Average Lease Term

WALT measures the average remaining lease duration across all tenants, weighted by their share of total rent. A WALT under 3 years signals re-leasing risk. It tells the lender that a significant portion of income could roll off in the near term, creating cash flow uncertainty. A WALT of 8 years or more signals stable, long-term income. That stability supports higher loan proceeds and better pricing.

Tenant concentration risk

- Identify the largest tenant’s rent share. If one tenant pays more than 25–30% of total rent, the lender flags it.

- Request tenant financials. Concentration above 25–30% triggers a full credit review of that tenant. The lender needs to know whether that tenant can sustain payments.

- Assess lease term alignment. If the dominant tenant’s lease expires before the loan matures, the lender treats that as a material risk.

- Evaluate replacement risk. The lender will ask: if this tenant leaves, how long does re-leasing take, and at what rent?

Tenant concentration is a primary focus in commercial lending because income dependency on a single source can collapse DSCR overnight. For investors holding multifamily properties in Connecticut or other supply-constrained markets, demonstrating tenant diversification is a direct path to better loan terms.

Effective rent vs. nominal rent

Lenders do not underwrite to the lease rate alone. They calculate effective rent by amortizing concessions across the lease term. A tenant paying $2,500 per month with two months of free rent on a 12-month lease has an effective rent of $2,083 per month. Concessions must be amortized into effective rent for underwriting purposes. Failing to disclose them upfront causes lenders to recalculate income downward after the fact.

What red flags in a rent roll slow lender review?

Lenders process dozens of loan packages simultaneously. A rent roll with problems does not get resolved quickly. It gets set aside. Knowing what triggers delays protects your timeline and your deal.

Common red flags include:

- Stale data. Lenders require rent rolls updated within 30 days of loan application. A rent roll from 90 days ago tells the lender nothing about current occupancy.

- Rents above market by 20% or more. When stated rents exceed comparable market rents by that margin, lenders apply market rent in their DSCR calculations instead of contract rent. That can reduce your qualifying income significantly.

- Missing lease copies. A rent roll without supporting lease documents is unverifiable. Lenders will not take the numbers at face value.

- Undisclosed concessions. Free rent periods buried in lease addenda and not reflected on the rent roll create reconciliation problems during underwriting.

- Inconsistent formatting. Handwritten notes, merged cells, and missing columns signal disorganized management. That perception carries into the lender’s risk assessment.

- Discrepancies with bank deposits. Rent rolls show contracted rent, not necessarily collected rent. Lenders cross-reference rent roll totals against 12 months of bank statements. Gaps between the two raise collection risk concerns.

Pro Tip: Run your own reconciliation before submitting. Pull 12 months of bank deposits and match them against your rent roll totals. If there are gaps, prepare a written explanation. Lenders respond better to disclosed discrepancies than discovered ones.

How should investors prepare a rent roll for lender review?

A well-prepared rent roll is a negotiation tool. It shapes how lenders perceive your property’s income quality and management competence. These steps produce a rent roll that moves through underwriting without delays.

- Update within 30 days of application. Stale rent rolls cause automatic delays. Date-stamp the document and confirm it reflects current occupancy.

- Use consistent column structure. Include unit number, tenant name, lease start date, lease end date, monthly rent, security deposit, concessions, ancillary income, and occupancy status. Every column should have data or a clear “N/A.”

- Attach all lease copies. Every tenant on the rent roll needs a corresponding executed lease. Include any addenda that modify rent, term, or concessions.

- Include tenant estoppels where available. Estoppels confirm lease terms directly from tenants and carry significant weight in commercial underwriting.

- Add market rent comparisons. Show comparable rents from nearby properties. If your rents are below market, this demonstrates upside. If they are at market, it confirms sustainability.

- Explain every vacancy. Note whether a vacant unit is being renovated, is actively marketed, or has a signed lease pending move-in. Unexplained vacancies look like chronic problems.

- Prepare a rent roll forward. Institutional underwriting expects a 90-day leasing pipeline showing upcoming renewals, move-outs, and new leases. This document validates income projections and demonstrates active management.

For investors pursuing a cash-out refinance on a stabilized rental property, a complete rent roll package often determines whether the lender underwrites to current income or applies a conservative stress scenario. The difference can be tens of thousands of dollars in loan proceeds.

Key Takeaways

A clean, current rent roll is the single most effective document an investor can submit to accelerate lender underwriting and maximize loan proceeds.

| Point | Details |

|---|---|

| Update within 30 days | Lenders reject stale rent rolls; date-stamp and refresh before every loan submission. |

| DSCR depends on effective rent | Amortize concessions into effective rent or lenders will recalculate income downward. |

| Vacancy above 25% triggers scrutiny | Keep vacancy documented and explained; lenders model a minimum 5% vacancy floor regardless. |

| Tenant concentration above 25–30% requires credit review | Diversify tenant income or prepare detailed financials for dominant tenants. |

| A 90-day rent roll forward strengthens underwriting | Show leasing pipeline to validate income projections and demonstrate active management. |

The rent roll is your first impression with a lender

After years of working with real estate investors across New England and Florida, I have seen one pattern repeat itself: investors who treat the rent roll as a formality lose money on their loan terms. Investors who treat it as a presentation win.

The rent roll is not proof of cash received. It is a record of contractual obligations. Lenders know this. They will verify actual collections through bank statements regardless of what the rent roll says. The investors who get the best outcomes are the ones who reconcile those two data sources themselves before submitting, then explain any gaps in writing.

I have also seen investors get caught off guard by tenant concentration risk. A six-unit building where one commercial tenant pays 40% of the rent looks strong on paper until that tenant’s lease expires in 18 months. Lenders see that immediately. Investors who address it proactively, by showing the tenant’s financials or a signed renewal letter, keep the deal moving. Those who ignore it watch their loan get restructured at closing.

The most underused tool in rent roll preparation is the market rent comparison. Showing a lender that your rents are 10% below market does not hurt your loan. It helps it. It tells the underwriter that income has room to grow and that the property is not dependent on above-market tenants to sustain cash flow. That is a risk reducer, not a weakness.

— Joe

Financing built around your rent roll

Investor MultiFamily Capital underwrites DSCR loans based on property cash flow, not personal income. That means your rent roll is the center of the underwriting conversation, not a supporting document.

Investor MultiFamily Capital reviews rent rolls for multifamily, fourplex, and single-tenant investment properties across Massachusetts, New Hampshire, Rhode Island, Connecticut, Maine, and Florida. Whether you are refinancing a stabilized asset or financing a value-add acquisition, the team evaluates your rent roll the same way an institutional lender does. Learn more about DSCR loan qualification or review your specific scenario with the team. Ready to move? Submit a Deal or Apply Online at investormultifamily.com/dscr-loans.

FAQ

What is a rent roll in real estate?

A rent roll is a document listing each tenant, unit, monthly rent, lease dates, and occupancy status for a rental property. Lenders use it to verify income and assess risk during loan underwriting.

Why do lenders require a current rent roll?

Lenders require rent rolls updated within 30 days of loan application because occupancy and rent levels can change quickly. Stale data produces inaccurate income projections and delays underwriting.

What is WALT and why does it matter to lenders?

WALT stands for Weighted Average Lease Term. A WALT under 3 years signals re-leasing risk; a WALT of 8 years or more indicates stable, long-term cash flow that supports larger loan proceeds.

How does tenant concentration affect loan approval?

When a single tenant accounts for more than 25–30% of total rent, lenders require a detailed credit review of that tenant. High concentration increases income dependency risk and can reduce loan proceeds.

Does a rent roll prove rental income to a lender?

A rent roll shows contracted rent, not collected rent. Lenders cross-reference rent roll totals against bank statements to confirm actual collections, so discrepancies between the two require written explanation.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.

Recommended

- Portfolio Lender Explained for Real Estate Investors | Investor MultiFamily Capital

- Rental Portfolio Financing | Investor MultiFamily Capital

- Short-Term Loan Terms Explained for Real Estate Investors | Investor MultiFamily Capital

- Midterm Rental Financing Explained for Investors | Investor MultiFamily Capital