TL;DR:

- Midterm rental financing uses DSCR loans to qualify investors through property cash flow rather than personal income. The appraiser’s Form 1007 market rent estimate caps the qualifying income, regardless of actual lease rents. This approach offers lighter regulation and scalability for investors in New England and Florida.

Midterm rental financing is a property cash flow lending approach that qualifies investors for loans on furnished rentals leased between one and six months. Unlike conventional mortgages, these loans use the Debt Service Coverage Ratio (DSCR) to evaluate the property’s income against its debt obligations. Personal W-2s and tax returns play no role in qualification. For investors in New England and Florida, this structure opens doors that traditional lending closes, especially for self-employed borrowers or those with large existing portfolios. Understanding midterm rental financing explained in full means knowing how DSCR underwriting, Form 1007 appraisals, and local regulations interact.

What are the key features of midterm rental financing and DSCR loans?

Midterm rentals are furnished properties rented for 30 to 90 days, positioned between short-term vacation rentals and traditional annual leases. They attract traveling nurses, corporate relocations, and remote workers who need a furnished home for a defined period. That tenant profile creates consistent demand without the nightly turnover of short-term rentals.

DSCR is the core metric in midterm lease financing options. The DSCR compares net operating income to annual debt service. A DSCR of 1.0 means the property’s income exactly covers its debt payments. Lenders typically require a DSCR of 1.2 or higher to build in a cushion for vacancies and unexpected expenses. That buffer matters because midterm properties carry higher operating costs than unfurnished rentals.

DSCR loans are non-QM investor loans that qualify based on property cash flow, not personal income documentation. This separates them from conventional mortgages, which require W-2s, tax returns, and debt-to-income calculations. For investors with multiple financed properties or self-employment income, DSCR loans remove the ceiling that conventional lending imposes.

Key features of DSCR loans for midterm rental investment:

- No personal income verification. Qualification depends entirely on the property’s projected rent versus debt service.

- Form 1007 appraisal. Lenders use an appraiser’s market rent estimate, not the actual signed lease, as the qualifying income figure.

- Portfolio scalability. DSCR loans have no portfolio caps, allowing investors to finance multiple properties simultaneously.

- Loan types. Products include purchase loans, cash-out refinances, and rate-and-term refinances on investment properties.

- Property types. Single-family, small multifamily, and condos qualify, subject to lender guidelines.

Pro Tip: Request the Form 1007 rent schedule from your appraiser before closing. If the appraised market rent comes in below your actual lease rate, your DSCR qualification will be capped at the lower figure regardless of what tenants are paying.

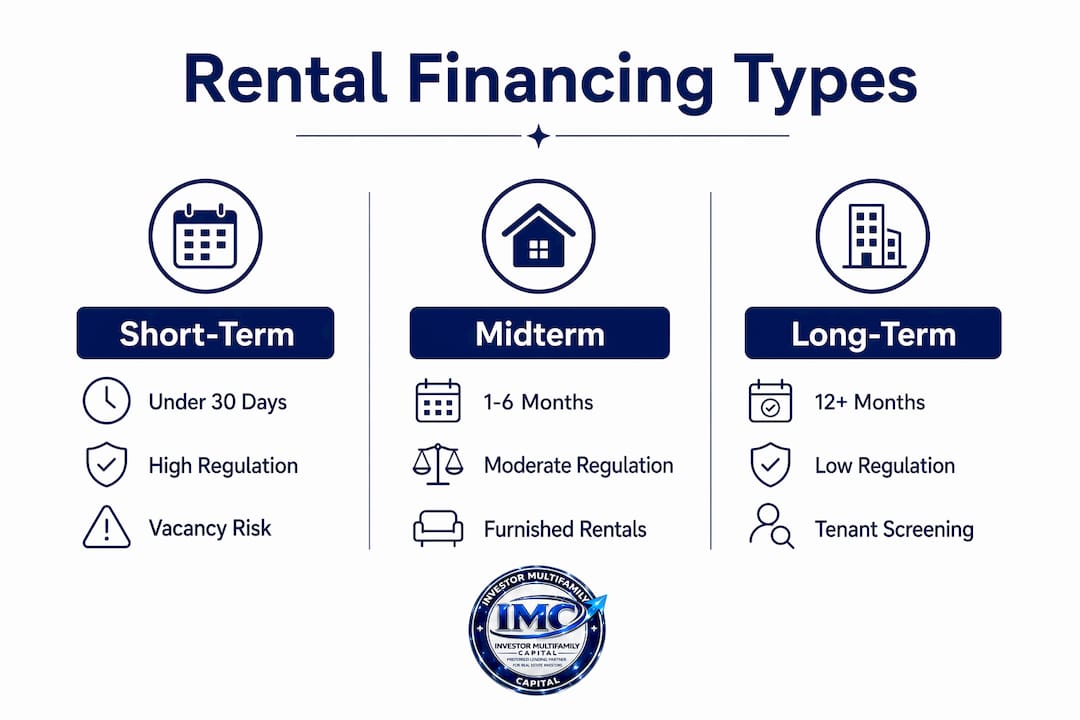

How does midterm rental financing differ from short-term and long-term rental financing?

The three rental categories carry distinct underwriting profiles. Knowing where midterm sits helps investors choose the right financing product and set realistic expectations.

| Factor | Short-term (under 30 days) | Midterm (1–6 months) | Long-term (12+ months) |

|---|---|---|---|

| Regulation intensity | Heavy | Light | Light |

| Turnover complexity | High | Moderate | Low |

| Income verification | Occupancy data, STR history | Form 1007 market rent | Lease or personal income |

| HOA/zoning risk | High | Moderate | Low |

| Furnishing requirement | Yes | Yes | No |

| DSCR qualification | STR income schedules | Appraised market rent | Lease income or personal income |

Short-term rentals under 30 days face the most regulatory friction. Cities across Massachusetts, Connecticut, and Florida have imposed licensing requirements, occupancy taxes, and outright bans in certain zones. Lenders financing short-term rentals often require documented STR income history and platform data from Airbnb or Vrbo to support underwriting.

Long-term rentals with 12-month leases rely more heavily on tenant income verification and, in some conventional products, borrower personal income. The underwriting is simpler but the income upside is lower. Unfurnished long-term rentals typically generate less gross rent than furnished midterm units in the same market.

Midterm rentals avoid complex STR regulations while earning more than unfurnished long-term rentals. The trade-off is that lenders use appraised market rent rather than actual lease income for DSCR calculations. Investors must understand that a higher actual rent does not automatically improve loan qualification if the appraiser’s Form 1007 estimate is lower.

Midterm financing also carries lighter HOA and zoning exposure than short-term rentals. Most HOA restrictions target nightly or weekly rentals. A 30-day minimum lease typically satisfies HOA rules in most jurisdictions, though investors should confirm this before acquisition.

What underwriting strategies maximize midterm rental loan approval?

Loan approval for midterm rental financing depends on one number above all others: the appraised market rent from Form 1007. Investors who understand this structure their entire acquisition and presentation strategy around it.

-

Pull comparable midterm leases before the appraisal. Appraisers rely on market data. Providing furnished rental comps in the same submarket gives the appraiser evidence to support a higher market rent estimate. Comps from Furnished Finder, corporate housing platforms, and local property managers all carry weight.

-

Invest in furnishing quality before the appraisal. A well-furnished property with quality appliances, fast internet, and functional workspace commands higher market rent. Appraisers assess the property as presented. A bare or poorly furnished unit will receive a lower rent estimate.

-

Include utilities and services in your rent model. Midterm tenants expect utilities, internet, and sometimes cleaning services included in rent. When these are bundled, the gross rent figure rises, which supports a higher appraised market rent and a stronger DSCR calculation.

-

Model vacancy conservatively. Lenders and appraisers apply a vacancy factor to gross market rent. Assume 10–15% vacancy in your DSCR model even if your actual occupancy is higher. A conservative model that still clears 1.2 DSCR is more credible to underwriters than an optimistic one that barely passes.

-

Do not rely on signed leases as the qualifying income source. A common pitfall is relying solely on signed leases for DSCR qualification. Lender workflows prioritize the appraiser’s market rent estimate from Form 1007. A signed lease at above-market rent does not override the appraiser’s figure.

Pro Tip: Structure your midterm rental business plan to qualify at appraised market rent, then realize higher actual rents as your operating upside. This approach, supported by Form 1007NSB appraisal forms, keeps your financing solid while your cash-on-cash return exceeds the underwriting assumption.

Qualifying for a DSCR loan requires understanding that the appraiser’s rent estimate is the ceiling for qualification purposes. Investors who present strong comps, well-furnished properties, and conservative expense models consistently achieve better outcomes than those who rely on actual lease income alone.

What costs, risks, and regulations affect midterm rental financing?

Operating costs for midterm rentals are higher than for unfurnished long-term rentals. Typical expenses include furniture depreciation, utilities, cleaning, insurance, and vacancy. These costs reduce net operating income and, by extension, the DSCR. Investors who underestimate expenses often find their DSCR falls below lender minimums after the first year.

Key cost and risk factors to model before financing:

- Furniture depreciation. Furnished units require ongoing replacement of appliances, linens, and furniture. Budget this as an annual expense line.

- Utilities. Midterm tenants expect utilities included. Monthly utility costs vary significantly by property size and climate.

- Cleaning and turnover. Each tenant transition requires professional cleaning. Budget per-turnover costs based on unit size.

- Platform and management fees. Listing platforms and property managers charge fees that reduce gross income.

- Vacancy. Even low-vacancy markets experience gaps between tenants. Model at least one vacant month per year per unit.

| Expense category | Impact on DSCR | Mitigation approach |

|---|---|---|

| Furniture depreciation | Reduces NOI | Capitalize and depreciate over useful life |

| Utilities | Reduces NOI | Bundle into rent; monitor monthly usage |

| Cleaning and turnover | Reduces NOI | Negotiate fixed-rate cleaning contracts |

| Vacancy | Reduces effective gross income | Model conservatively; target corporate tenants |

| Platform fees | Reduces gross income | Negotiate direct leases where possible |

Midterm rental income follows standard rental income tax treatment in most cases. Hotel occupancy taxes, which apply to short-term rentals in many states, generally do not apply to stays of 30 days or longer. Massachusetts, Connecticut, and Florida each have specific thresholds, so investors should confirm local rules before assuming tax exemption.

Zoning and HOA rules are lighter for midterm rentals than for short-term rentals, but they are not absent. Some municipalities require a rental registration or business license even for 30-day-minimum rentals. Investors in New England markets should verify local ordinances before acquisition, not after.

Key takeaways

Midterm rental financing qualifies investors based on property cash flow through DSCR loans, with the appraiser’s Form 1007 market rent estimate serving as the authoritative qualifying income figure.

| Point | Details |

|---|---|

| DSCR is the qualifying metric | Lenders require a DSCR of 1.2 or higher; income must exceed debt service by a meaningful margin. |

| Form 1007 sets the income ceiling | Actual lease income above appraised market rent does not improve DSCR qualification. |

| Midterm regulation is lighter | Midterm rentals avoid most STR licensing and hotel tax rules, but local zoning checks are still required. |

| Operating costs reduce NOI | Furniture, utilities, cleaning, and vacancy must be modeled before running DSCR calculations. |

| DSCR loans scale without income caps | Self-employed investors and those with large portfolios qualify based on property cash flow, not personal income. |

What I have learned about midterm rental financing in 2026

Investors consistently underestimate how much the Form 1007 appraisal controls their financing outcome. The most common mistake I see is an investor who signs a midterm lease at a strong rent, then expects that lease to drive their DSCR calculation. It does not. The appraiser’s market rent estimate is what the lender uses, full stop.

The midterm rental market in 2026 offers real cash flow advantages over both short-term and long-term rentals in the right markets. Corporate relocation demand in markets like Boston, Providence, and Tampa remains strong. But the financing only works when investors align their underwriting assumptions with what appraisers will actually support.

DSCR financing is the right product for scaling a midterm rental portfolio. It removes personal income as a constraint, which matters enormously for investors who are already at conventional loan limits. The key is disciplined financial modeling: conservative vacancy, realistic expense loads, and a property presentation that supports the highest defensible appraised market rent. Investors who get that right build portfolios that perform on paper and in practice.

— Joe

Financing midterm rentals with Investor MultiFamily Capital

Investor MultiFamily Capital specializes in business-purpose DSCR loans for real estate investors across New England and Florida. Whether you are acquiring your first midterm rental or refinancing an existing portfolio, the underwriting focuses on property cash flow, not your personal tax returns.

Investor MultiFamily Capital offers DSCR loan products structured for investment properties including midterm rentals, multifamily assets, and short-term rental units. Investors in Massachusetts, Connecticut, Maine, New Hampshire, Rhode Island, and Florida can apply for DSCR financing directly through the platform. Submit a Deal, Run Deal Analysis, or Apply Online to get your midterm rental scenario reviewed by an experienced investment property lender.

FAQ

What is midterm rental financing?

Midterm rental financing is a lending approach that uses DSCR loans to qualify investors based on property cash flow from furnished rentals leased for 30 days to six months. Personal income documentation is not required for qualification.

How does a lender calculate DSCR for a midterm rental?

The lender divides the property’s net operating income by its annual debt service. The qualifying income figure comes from the appraiser’s Form 1007 market rent estimate, not the actual signed lease.

What DSCR do lenders require for midterm rental loans?

Lenders typically require a DSCR of 1.2 or higher to provide a cushion for vacancies and unexpected operating expenses.

Can my actual midterm rent improve my loan qualification?

Not automatically. Actual higher midterm rents may not improve loan qualification if the appraiser’s Form 1007 estimate is lower. The appraised market rent is the ceiling for DSCR calculation purposes.

Do midterm rentals face the same regulations as short-term rentals?

No. Midterm rentals generally face lighter regulation than short-term rentals and are not subject to hotel occupancy taxes in most jurisdictions. Investors should still verify local zoning, HOA rules, and any rental registration requirements before acquisition.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.