TL;DR:

- Proper flip deal analysis involves calculating the maximum allowable offer by itemizing all costs and using condition-matched ARVs. Investors who run full analysis and stress-test projections avoid overpaying and protect their profit margins. Relying solely on quick rules like the 70% rule leads to overestimating deal value and potential losses.

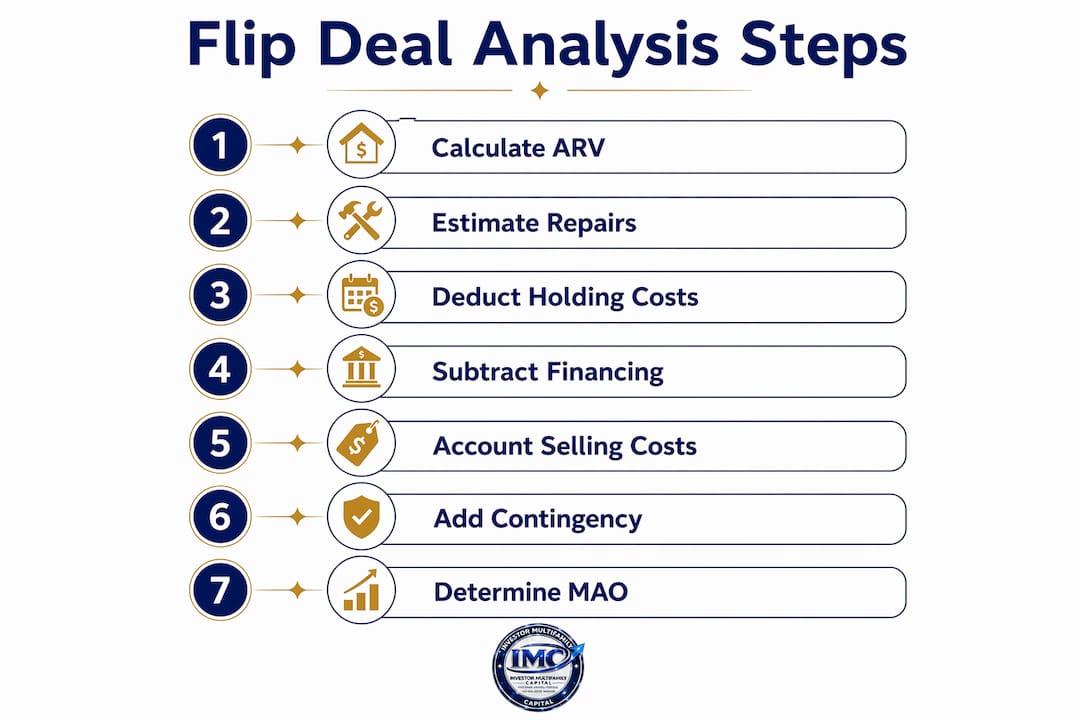

Flip deal analysis is defined as the process of calculating the maximum price you can pay for a property while still hitting your profit target after every cost is accounted for. The industry term for this ceiling is the maximum allowable offer, or MAO. Knowing how to analyze flip deals separates investors who build repeatable businesses from those who gamble on best-case scenarios. The 70% rule gives you a fast screen, but serious fix-and-flip analysis requires itemizing every acquisition, rehab, holding, financing, and selling cost. Net profit targets of $25,000–$30,000 and ROI expectations of 15–20% are standard benchmarks among successful investors. Miss one cost category and your margin disappears before you close.

How to analyze flip deals: the MAO framework

The maximum allowable offer is the single most important number in any flip deal evaluation. Every other calculation feeds into it. The formula forces you to work backward from your after-repair value (ARV), subtract all costs, and subtract your required profit. What remains is the most you can pay for the property.

The 70% rule is the fastest version of this calculation:

MAO = (ARV × 70%) minus repair costs

A property with a $300,000 ARV and $50,000 in repairs produces an MAO of $160,000 under the 70% rule. That 30% buffer is meant to cover selling costs, holding costs, and profit. The problem is that 30% is a rough average. In high-cost markets or on deals with long timelines, 30% is not enough. The 70% rule works as a quick screen to eliminate bad deals fast. It does not replace a full itemized analysis.

The itemized MAO formula is:

MAO = ARV minus repairs minus holding costs minus financing costs minus selling costs minus contingency minus minimum profit

Run this formula on every deal before making an offer. The result tells you exactly what you can pay and still hit your return target.

| Scenario | ARV | Repair Estimate | 70% Rule MAO | Itemized MAO | Difference |

|---|---|---|---|---|---|

| Deal A | $300,000 | $50,000 | $160,000 | $148,000 | $12,000 |

| Deal B | $400,000 | $80,000 | $200,000 | $183,000 | $17,000 |

| Deal C | $250,000 | $40,000 | $135,000 | $121,000 | $14,000 |

The itemized MAO consistently comes in lower than the 70% rule estimate. That gap represents real costs the quick formula ignores. Investors who use only the 70% rule routinely overpay.

Pro Tip: Run the itemized MAO formula first. Use the 70% rule only to decide whether a deal is worth the time to build the full analysis.

What are the essential cost components in flip deal analysis?

Every cost category below the purchase price directly reduces your profit. Missing even one can turn a winning deal into a loss.

Acquisition costs

- Purchase price

- Buying closing costs: typically 1–3% of the purchase price, covering title, escrow, and lender fees

Rehab costs

- Line-item scope of work for every trade: demo, framing, electrical, plumbing, HVAC, roofing, finishes

- 10–15% contingency added on top of the base rehab estimate to cover hidden defects

Holding costs

- Property taxes prorated monthly

- Hazard insurance

- Utilities: electric, gas, water

- HOA fees if applicable

- Loan interest accruing during the project

Financing costs

- Hard money or fix-and-flip loan interest for the full projected hold period

- Origination points paid at closing, typically 1–3 points on the loan amount

- Understanding real estate leverage helps you model these costs accurately before you commit

Selling costs

- Agent commissions and closing fees: 7–10% of ARV is the standard range

- Transfer taxes and recording fees

- Staging and professional photography

Pro Tip: Build your cost sheet in a spreadsheet before you visit the property. Fill in estimates as you gather information. Never leave a line item blank.

Why accurate ARV and comp matching are critical

ARV is the single variable with the most leverage over your deal outcome. A $20,000 error in ARV on a $300,000 deal shifts your MAO by the same amount. Overestimate ARV and you overpay for the property. Underestimate it and you pass on a profitable deal.

Selecting the right comparable sales requires matching four factors: square footage within 10–15%, similar bedroom and bathroom count, same neighborhood or street pattern, and sales within the last 90 days. Recency matters because markets shift. A comp from eight months ago in a cooling market will inflate your ARV estimate.

The most frequent ARV estimation error comes from mixing renovated and unrenovated comps without making condition adjustments. A fully renovated sale and a dated original-condition sale in the same neighborhood can differ by $40,000 or more. Using both without adjustment produces a blended ARV that reflects neither property accurately.

Proper comp condition matching requires reviewing listing photos rather than relying solely on data points. MLS data tells you the sale price. The photos tell you whether that sale had new kitchen cabinets, updated bathrooms, and fresh flooring. Your flip will compete with renovated properties, so your comps must reflect that standard.

- Pull 3–5 sold comps within 90 days

- Confirm each comp is fully renovated by reviewing listing photos

- Adjust for size differences using a price-per-square-foot calculation

- Exclude any comp that is not condition-matched to your planned finish level

- Use the median of your adjusted comps, not the highest sale

Consequences of poor ARV assumptions extend beyond a single deal. Investors who consistently overestimate ARV develop a false sense of deal quality. They close on properties that cannot sell at the price the analysis assumed, and they absorb losses that erode their capital base.

How to budget for realistic repair costs and timelines

Rehab budgets built on rough guesses produce costly surprises. Line-item scopes with a 10–15% contingency added on top are the standard for serious investors. The contingency covers hidden electrical issues, water damage discovered behind walls, and permit requirements that were not visible during the initial walkthrough.

Build your scope of work room by room, trade by trade, even before you have contractor bids. Use your knowledge of local labor and material costs to assign rough numbers to each line. The goal is not precision at this stage. The goal is to identify every work category so nothing gets missed when bids come in.

- Walk the property with a checklist covering roof, foundation, HVAC, electrical panel, plumbing, windows, and all interior finishes

- Assign a cost range to each item based on local market rates

- Total the base estimate and add 10–15% contingency

- Get at least two contractor bids to validate your estimate before closing

Timeline assumptions are where most investors lose money quietly. Experienced flippers budget 5–7 months for the full project, including renovation and time on market. Beginners often assume 2–3 months. That gap of 3–4 months represents $6,000–$20,000 in additional carrying costs at typical rates.

Carrying costs average $2,000–$5,000 per month depending on the market and loan balance. Multiply your monthly carrying cost by your projected hold time and add that number to your cost sheet. Then stress-test the deal by adding one extra month to your timeline and dropping your ARV by 5–10%. If the deal still works, you have real margin. If it breaks, the deal depends on perfect conditions.

Pro Tip: Never model only the best case. Run a downside scenario with ARV 10% lower and hold time 3 months longer before you make an offer. If the deal still pencils, proceed. If it does not, pass.

Downside modeling is not pessimism. It is the standard practice that separates investors who build wealth from those who break even over years of work. A deal that only works under perfect conditions is a deal that should not be funded.

Key Takeaways

Accurate flip deal analysis requires a complete itemized MAO formula, condition-matched ARVs, realistic timelines of 5–7 months, and a 10–15% rehab contingency to protect your profit margin.

| Point | Details |

|---|---|

| Use the itemized MAO formula | Calculate MAO by subtracting all costs and required profit from ARV, not just repairs. |

| Match comps by condition | Review listing photos to confirm every comp reflects a fully renovated finish level. |

| Budget 5–7 months hold time | Experienced investors plan for longer timelines to avoid underestimating carrying costs. |

| Add 10–15% rehab contingency | Hidden defects, permit issues, and scope changes make contingency non-negotiable. |

| Run a downside scenario | Stress-test every deal with lower ARV and extended hold time before committing capital. |

What I’ve learned from watching investors skip the hard math

Speed is the enemy of accurate flip deal analysis. I have watched investors rush through comp selection, accept a contractor’s verbal estimate as the budget, and assume a 90-day flip timeline because that is what they hoped for. Most of those deals ended with thin returns or outright losses.

The investors who build consistent track records do one thing differently. They treat every deal as if the worst case is the base case. They pass on deals with slim margins that require everything to go right. That discipline feels conservative in a hot market. It feels like genius when a renovation runs long or a buyer falls through.

Poor comp selection is the most common mistake I see. Investors pull the three highest sales in a neighborhood without checking whether those properties were fully renovated. They build an ARV on sales that do not reflect what their finished product will compete against. The fix is simple: open every comp’s listing photos before you record the sale price.

The other pattern I see is optimism bias on timelines. Investors who have never done a full gut renovation assume they will finish in 10 weeks. Permits alone can add 4–6 weeks in many New England markets. A disciplined, repeatable analysis framework that includes itemized costs and contingency planning is what separates successful flippers from those who are perpetually surprised by the outcome.

My advice: build your deal analysis template once, use it on every deal, and never make an offer without completing every line. The deals that look great on a napkin calculation rarely survive a full itemized analysis. The ones that survive the full analysis are worth pursuing.

— Joe

Financing your next flip with Investor MultiFamily Capital

Accurate deal analysis tells you what to pay. The right financing determines whether you can close fast enough to get the deal.

Investor MultiFamily Capital provides fix-and-flip loans built for business-purpose investors across New England and Florida. Underwriting is based on the property and the deal, not your personal income. Closings move fast, which matters when you are competing for off-market properties or distressed assets with motivated sellers. Investors in MA, NH, RI, CT, ME, and FL can Submit a Deal directly or Apply Online to get a financing decision on their next flip. Run your deal analysis first, then bring the numbers to Investor MultiFamily Capital.

FAQ

What is the 70% rule in flip deal analysis?

The 70% rule states that your maximum offer equals 70% of ARV minus estimated repair costs. It is a quick screening tool, not a substitute for a full itemized cost analysis.

What net profit should a flip deal target?

Successful investors target net profit of $25,000–$30,000 per deal and an ROI of 15–20% after all costs. Deals below these thresholds carry too little margin to absorb setbacks.

How long should I budget for a flip project?

Budget 5–7 months for the full project, including renovation and time on market. Experienced flippers use this range rather than the optimistic 2–3 month assumption that beginners often apply.

Why do ARV errors cause the most damage in flip analysis?

ARV errors shift your MAO dollar for dollar. A $20,000 overestimate in ARV means you pay $20,000 too much for the property, which directly reduces your net profit by the same amount.

What contingency should I add to my rehab budget?

Add 10–15% on top of your base rehab estimate to cover hidden defects, permit requirements, and scope changes discovered during renovation.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.