TL;DR:

- Portfolio lenders retain mortgage loans on their own balance sheets, offering manual underwriting and flexible property eligibility. They provide faster closing times, higher leverage for complex assets, and accommodate more properties than conventional GSE lenders, but often charge higher rates and require larger reserves. These lenders are ideal for investors with non-standard income, multiple properties, or tricky assets, emphasizing long-term relationships and negotiated exit terms.

A portfolio lender is a bank, credit union, or private lending institution that originates mortgage loans and keeps them on its own balance sheet rather than selling them to the secondary market. That single operational difference unlocks underwriting flexibility that Fannie Mae and Freddie Mac guidelines simply do not allow. For real estate investors working with complex income structures, non-warrantable properties, or growing rental portfolios, understanding how portfolio lenders work is often the difference between closing a deal and losing it.

How portfolio lenders work vs. conventional lenders

Portfolio lenders originate and retain loans on their own balance sheet, which means they set their own underwriting criteria. Conventional lenders, by contrast, originate loans with the intent to sell them to Fannie Mae or Freddie Mac. That sale requires strict conformance to agency guidelines, which leaves little room for manual judgment.

Conventional loans run through automated underwriting systems like Fannie Mae’s Desktop Underwriter (DU) and Freddie Mac’s Loan Prospector (LP). These systems produce eligibility recommendations based on standardized criteria: debt-to-income ratios, credit score thresholds, property type classifications, and financed property counts. If a borrower or property falls outside those parameters, the system declines the file. There is no room for context.

Portfolio lenders replace that automated process with manual, holistic review. An underwriter evaluates the full picture: rental income history, asset reserves, property cash flow, entity structure, and the lender’s own risk appetite. That review path is slower in some cases but far more accommodating for investors with complex documentation.

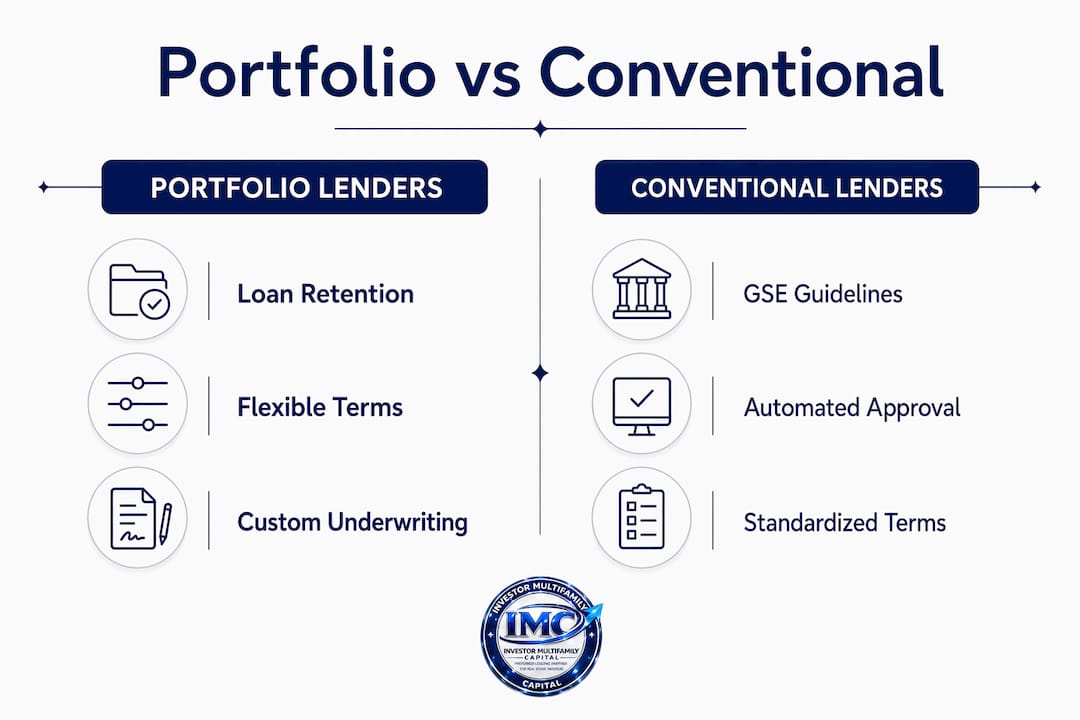

Here is how the two approaches differ operationally:

- Loan retention. Portfolio lenders hold the loan. Conventional lenders sell it. That retention is what drives every other difference.

- Underwriting criteria. Portfolio lenders write their own guidelines. Conventional lenders follow GSE checklists.

- Income documentation. Portfolio lenders accept bank statements, rental schedules, and entity returns. Conventional lenders typically require W-2s and standard tax returns.

- Property eligibility. Portfolio lenders can finance mixed-use buildings, non-warrantable condos, and properties with deferred maintenance. Conventional lenders cannot.

- Closing speed. Portfolio loans can close in approximately 21–30 days versus 45–60 days for conventional investment loans. That speed reflects fewer compliance layers, not less diligence.

Pro Tip: When approaching a portfolio lender, bring a complete loan package upfront: rent rolls, operating statements, entity documents, and a 12-month bank statement. Manual underwriters move faster when the file is clean.

What are the benefits and drawbacks of portfolio loans?

Portfolio lending benefits are most visible when a conventional loan is not an option. The core advantage is approval access for scenarios that automated systems reject outright.

Key benefits for real estate investors:

- Flexible income documentation. Self-employed investors, LLC borrowers, and those with multiple depreciation schedules can present their actual financial picture rather than a tax-return summary that understates income.

- Non-standard property types. Mixed-use buildings, large multifamily assets, and properties with title complications are all candidates for portfolio financing.

- No financed property caps. Conventional GSE guidelines limit financed investment properties to approximately 10 under specific conditions. Portfolio lenders underwrite beyond that ceiling.

- Custom loan structures. Interest-only periods, balloon terms, and adjustable rate structures are negotiable with portfolio lenders. Conventional products offer far less flexibility.

- Faster execution. For time-sensitive acquisitions, the 21–30 day closing window is a real operational advantage.

Trade-offs investors must price in:

- Higher interest rates. Portfolio loans carry rates approximately 1–2 percentage points above comparable conventional loans. That spread reflects the lender’s retained credit risk.

- Larger down payments. Expect 25–30% down on investment properties, with some lenders requiring more for complex assets.

- Reserve requirements. Portfolio lenders typically require 6–12 months of reserves per property, sometimes across the entire portfolio.

- Origination fees. Points and origination costs tend to run higher than conventional products.

The rate premium is real but often irrelevant when the alternative is no financing at all. Investors scaling beyond 10 properties or financing non-standard assets have no conventional option to compare against.

Which borrowers and properties benefit most from portfolio lending?

Portfolio lending is not a universal solution. It performs best in specific scenarios where conventional guidelines create a hard stop.

| Borrower or Property Scenario | Why Portfolio Lending Fits |

|---|---|

| Self-employed investor with high depreciation | Bank statements or P&L accepted instead of tax returns |

| Investor with 10+ financed properties | No GSE property count limits apply |

| Non-warrantable condo or mixed-use asset | Portfolio lenders set their own property eligibility rules |

| Recent credit event (bankruptcy, foreclosure) | Manual review weighs compensating factors like reserves and cash flow |

| High-net-worth borrower with complex asset structure | Holistic review of total financial picture, not just income ratios |

| DSCR-focused rental investor | Property cash flow drives approval, not personal income |

Portfolio lenders evaluate compensating factors like rental income, asset reserves, and overall financial resilience rather than relying on rigid eligibility checklists. That manual review path is what makes them viable for investors whose profiles look complicated on paper but are financially sound in practice.

For investors using entity structures like LLCs or LPs, portfolio lenders are often the only institutional option. Conventional GSE products do not lend to entities for investment properties in most cases. Portfolio lenders underwrite the entity, the guarantor, and the asset together.

How do portfolio loans interact with DSCR strategies?

DSCR (Debt Service Coverage Ratio) is a property-level underwriting metric. It measures whether a property’s net operating income covers its debt service. A DSCR above 1.0 means the property generates enough cash flow to cover the loan payment. Portfolio lending is the structural framework. DSCR is one underwriting method that portfolio lenders frequently apply.

Portfolio lenders and DSCR programs can be combined strategically for rental portfolio scaling. A portfolio lender using DSCR underwriting evaluates the property’s income rather than the borrower’s personal tax returns. That combination is particularly powerful for investors with 5, 10, or 20 rental properties who cannot document personal income at the level conventional lenders require.

Key considerations when layering DSCR underwriting with portfolio lending:

- Entity structuring. Most DSCR-focused portfolio lenders require loans to close in an LLC or other business entity. Confirm entity requirements before submitting a deal.

- DSCR minimums. Lender-specific DSCR thresholds vary. Some require 1.20x, others accept 1.0x or even below 1.0x with compensating factors. Know the floor before underwriting your deal.

- Reporting obligations. Some portfolio loan structures include ongoing financial reporting covenants. Understand what you are agreeing to before closing.

- Loan layering. Investors often use rental portfolio financing to consolidate multiple single-family rentals under one portfolio loan, simplifying debt management while preserving cash flow.

Pro Tip: Run your DSCR calculation before approaching a lender. Use gross rental income, subtract vacancy and operating expenses, then divide by annual debt service. A DSCR of 1.25x or higher gives you negotiating room on rate and terms.

You can also learn more about qualifying for a DSCR loan to understand what documentation and property metrics lenders prioritize.

What should investors know about pricing, terms, and loan servicing?

Pricing and structure on portfolio loans require careful review before signing. The flexibility that makes these loans attractive also creates room for terms that can cost you on the back end.

Rate and fee structure:

- Expect rates 1–2 points above conventional benchmarks, reflecting the lender’s retained credit risk.

- Origination fees of 1–3 points are common. Model total cost of capital, not just the note rate.

- Interest-only periods are available from many portfolio lenders and can improve cash-on-cash returns during a hold period.

Loan servicing:

- Portfolio lenders service their own loans in most cases. That means you deal directly with the lender for payments, escrow, and modifications. The experience is often more responsive than dealing with a large servicer.

- Loan modifications and extensions are more accessible with portfolio lenders because the decision-maker holds the note.

Exit mechanics:

- Complex release mechanics and covenants in some portfolio loan structures can make selling individual properties within a blanket loan more expensive than anticipated. Collateral release prices and prepayment penalties vary significantly by lender.

- Model your exit before you close. If you plan to sell one property out of a portfolio loan in year two, confirm the release price and any associated fees upfront.

The most overlooked cost in portfolio lending is not the rate. It is the exit. Investors who negotiate collateral release terms and prepayment structures before closing avoid expensive surprises during disposition.

Key takeaways

Portfolio lending gives real estate investors access to flexible, property-focused financing that conventional GSE guidelines cannot match, but it requires clean documentation, higher reserves, and careful review of exit terms.

| Point | Details |

|---|---|

| Portfolio lenders retain loans | Loan retention drives underwriting flexibility beyond Fannie Mae and Freddie Mac guidelines. |

| DSCR and portfolio lending intersect | Portfolio lenders frequently use DSCR underwriting to qualify investment properties on cash flow, not personal income. |

| Rates run 1–2 points higher | The rate premium reflects retained credit risk; model total cost of capital before comparing to conventional products. |

| GSE property limits do not apply | Investors with more than 10 financed properties must use portfolio or private lenders to continue scaling. |

| Exit terms require negotiation | Collateral release prices and prepayment penalties vary widely; negotiate these before signing. |

Why most investors underestimate portfolio lenders

I have seen investors treat portfolio lenders as a last resort, something you turn to only after a conventional lender says no. That framing is backwards. For serious investors scaling beyond a handful of properties, portfolio lenders are often the first call worth making, not the last.

The misconception I encounter most often is that portfolio loans are easier to get. They are not. Portfolio lenders underwrite credit risk manually and still require sound repayment ability. What they offer is a different evaluation path, one that weighs the full financial picture rather than running a file through an algorithm. That distinction matters enormously when your income comes from rental schedules, K-1s, or entity distributions rather than a W-2.

The investors who use portfolio lenders most effectively treat them as long-term relationships, not transactional vendors. A lender who knows your portfolio, your track record, and your documentation style will move faster and price more competitively on your fifth deal than on your first. Build that relationship before you need it urgently.

One more thing: always read the loan covenants. The flexibility that makes portfolio loans attractive can also produce complex exit mechanics that catch investors off guard. Negotiate release prices and prepayment terms before you close, not after you have a buyer under contract.

— Joe

Flexible investment financing from investor MultiFamily capital

Investor MultiFamily Capital structures business-purpose loans for real estate investors in Massachusetts, New Hampshire, Rhode Island, Connecticut, Maine, and Florida. If you are working with a non-standard property, a complex income profile, or a portfolio that has outgrown conventional guidelines, IMC offers DSCR loan products built around property cash flow rather than personal income. From multifamily acquisitions to BRRRR refinances and deal rescue scenarios, IMC underwrites the deal, not just the borrower. Review your scenario and Submit a Deal to see how IMC can structure financing for your next investment.

FAQ

What is a portfolio lender?

A portfolio lender is a bank, credit union, or private lender that originates mortgage loans and holds them on its own balance sheet rather than selling them to Fannie Mae or Freddie Mac. That retention allows the lender to set its own underwriting criteria and approve borrowers or properties that do not meet agency guidelines.

How do portfolio loans differ from conventional loans?

Conventional loans must conform to GSE guidelines and run through automated underwriting systems like Fannie Mae’s DU. Portfolio loans use manual, holistic underwriting that evaluates the full borrower and property profile, including rental income, reserves, and entity structure.

Are portfolio loan rates higher than conventional rates?

Portfolio loans typically carry interest rates approximately 1–2 percentage points above comparable conventional loans. That premium reflects the lender’s retained credit risk and the underwriting flexibility it provides.

Can portfolio lenders finance more than 10 properties?

Yes. Conventional GSE guidelines limit financed investment properties to approximately 10 under specific conditions. Portfolio lenders are not bound by those limits and can finance investors with larger rental portfolios.

Do portfolio lenders use DSCR underwriting?

Many portfolio lenders apply DSCR underwriting for investment properties, evaluating whether the property’s net operating income covers its debt service rather than relying on the borrower’s personal income documentation. DSCR describes the underwriting method; portfolio lender describes the loan retention structure. The two frequently work together.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.