TL;DR:

- STR loans are non-QM investment financing based on short-term rental income, not personal income verification.

- They primarily utilize DSCR calculations derived from third-party data, allowing faster closings of 10 to 21 days.

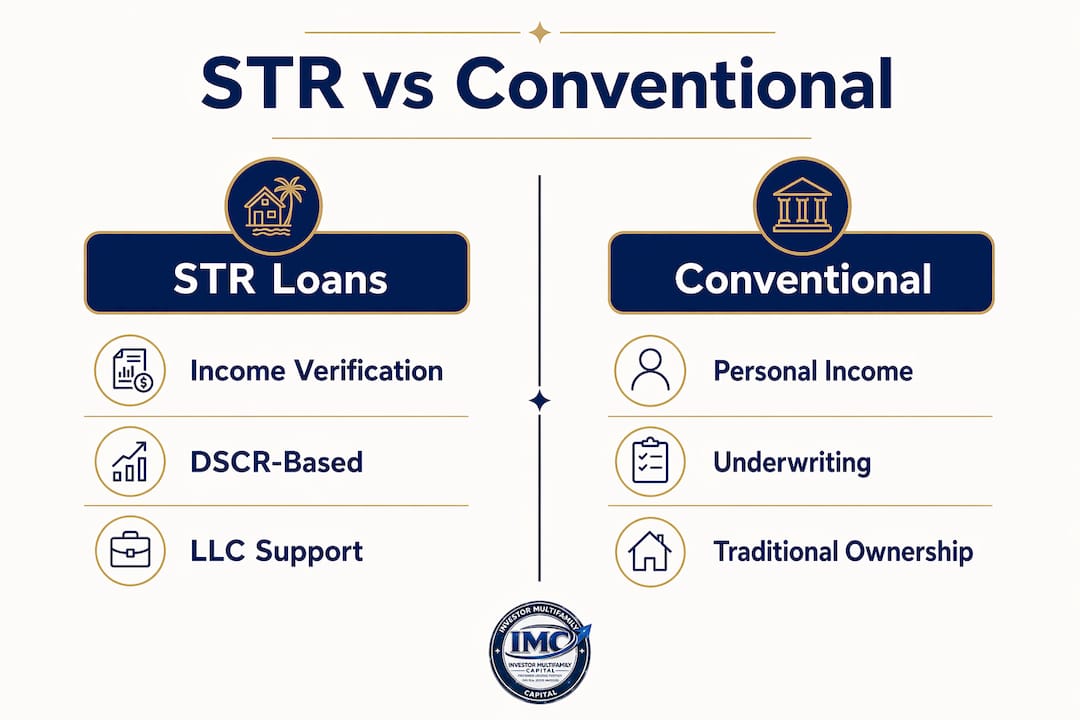

An STR loan is a non-QM investment loan that qualifies borrowers based on a property’s projected rental income rather than personal income verification, making it the primary financing tool for investors purchasing or refinancing short-term rental properties on platforms like Airbnb and VRBO. Unlike conventional investment loans, STR loans require no W-2s or tax returns. Underwriting centers on the Debt Service Coverage Ratio, or DSCR, calculated from rental income data sourced through tools like AirDNA. Closings typically complete in 10 to 21 days, giving investors a speed advantage in competitive markets.

What is an STR loan and how does it work?

An STR loan, formally categorized as a DSCR-based non-QM investment loan, is purpose-built for properties operated as short-term rentals. The core mechanic is straightforward: the lender evaluates whether the property generates enough rental income to cover its debt obligations, not whether the borrower earns a salary. This distinction matters enormously for investors who hold multiple properties, operate through LLCs, or show complex tax returns with significant depreciation write-offs.

The underwriting process relies on third-party income data. Lenders pull revenue projections from platforms like AirDNA, cross-reference appraisal rent schedules, and review any existing platform income statements from Airbnb or VRBO. The DSCR loan structure replaces the traditional income verification stack with a property-performance model. That shift is what makes STR financing accessible to investors who would otherwise be blocked by conventional debt-to-income limits.

STR loans also support entity-level ownership. Financing through LLCs with personal guarantees from principals is standard practice, giving investors the liability protection of a corporate structure without sacrificing loan eligibility. This is a structural advantage that conventional Fannie Mae or Freddie Mac products do not offer.

How do STR loans differ from conventional investment property loans?

The differences between STR loans and conventional investment property loans are significant across eligibility, documentation, and pricing.

| Feature | STR Loan (DSCR-Based) | Conventional Investment Loan |

|---|---|---|

| Income verification | Property rental income | Personal W-2 or tax returns |

| Entity ownership | LLC or corporation allowed | Typically requires personal title |

| Property limit | No cap on portfolio size | Often capped at 10 financed properties |

| Closing timeline | 10 to 21 days | 30 to 60 days |

| Interest rate range | 6.5% to 8.0% typical | Lower, based on personal credit profile |

| Income source used | Short-term rental projections | Long-term lease income |

The rate premium on STR loans reflects the reduced documentation and higher perceived income volatility. STR loan rates for well-qualified borrowers typically start around 6.0% and range between 6.5% and 8.0%. That premium over conventional loans is the cost of flexibility, and for most investors scaling a short-term rental portfolio, it is a worthwhile trade.

Key structural differences investors should understand before applying:

- No personal income verification or debt-to-income calculation

- Qualification based entirely on DSCR using projected or verified STR income

- Down payments typically range from 20% to 30% depending on DSCR and credit score

- Reserve requirements are higher than conventional loans, often 6 to 12 months of PITIA

- Investment property loan options vary by lender, so terms are not standardized across the market

What is the process for qualifying and obtaining an STR loan?

The STR loan application process is more focused than a conventional mortgage but still requires specific documentation. Investors who prepare their file in advance close faster and face fewer underwriting conditions.

-

Credit score review. Most STR lenders require a minimum credit score of 660 to 680. Scores above 720 typically unlock better rate tiers and lower down payment requirements.

-

Property identification and appraisal order. The lender orders an appraisal that includes a rent schedule comparing the subject property to similar local STR properties. This schedule forms the baseline for income projections.

-

Income documentation assembly. Lenders require third-party revenue reports, typically from AirDNA, and any available platform income statements from Airbnb or VRBO. New acquisitions rely entirely on projections; existing rentals can supplement with actual performance data.

-

Income discounting and DSCR calculation. Lenders apply a 20 to 40% discount to gross projected rental income to account for vacancy, platform fees, and seasonality. The discounted figure is then divided by total monthly debt service to produce the DSCR.

-

Regulatory and permit verification. In markets with active STR restrictions, such as Boston, Miami Beach, or Portland, lenders verify that the property holds or is eligible for an STR operating permit. Properties in STR-restrictive zones face additional scrutiny or denial.

-

Approval and closing. Once underwriting clears, loan processing runs 10 to 21 days from application to closing, significantly faster than conventional investment loans.

Pro Tip: Build your AirDNA revenue report and appraisal rent schedule before submitting your loan application. Lenders who receive complete documentation on day one move to approval faster. Gaps in income documentation are the single most common cause of underwriting delays on STR files.

How does DSCR influence STR loan approval and interest rates?

DSCR is the single most important number in STR loan underwriting. It is calculated by dividing gross rental income (after lender discounts) by total monthly debt service, which includes principal, interest, taxes, insurance, and any HOA dues.

| DSCR Level | Lender Interpretation | Typical Outcome |

|---|---|---|

| Below 1.0 | Property cash flow does not cover debt | Denial |

| 1.0 to 1.24 | Marginal coverage, higher risk | Approval possible, higher rate |

| 1.25 and above | Strong coverage, lower risk | Best rate tiers, smoother approval |

| 1.40 and above | Excellent coverage | Maximum pricing advantage |

The industry standard DSCR threshold for best pricing is 1.25x. Properties above this level qualify for the most favorable interest rate tiers and face fewer underwriting conditions. The minimum accepted DSCR is 1.0x, meaning the property’s discounted income must at least equal its total debt service.

Income discounting creates a critical math problem that many investors underestimate. If a property projects $6,000 per month in gross STR revenue and the lender applies a 30% discount, the underwritten income drops to $4,200. If total monthly debt service is $4,000, the DSCR is 1.05, which clears the minimum but misses the preferred 1.25x threshold. That gap translates directly into a higher interest rate.

Pro Tip: Run your DSCR calculation using the lender’s discounted income figure, not your gross projection. Apply a 30% haircut to your AirDNA estimate before modeling loan scenarios. If the resulting DSCR falls below 1.25x, consider a larger down payment to reduce monthly debt service and push DSCR above the preferred threshold.

A low DSCR after discounting is the most common reason for STR loan denial. Investors who model their deals using optimistic gross revenue figures without accounting for lender discounts frequently encounter this problem at the underwriting stage.

What challenges should STR loan investors prepare for?

STR loan underwriting carries specific hurdles that do not exist in conventional investment lending. Investors who understand these in advance avoid surprises at the closing table.

-

Reserve requirements. STR lenders require 6 to 12 months of PITIA in verified liquid assets after closing. This is substantially higher than the two to three months required on conventional investment loans. Seasonal income volatility and regulatory risk drive this requirement.

-

Regulatory exposure. Cities including Santa Monica, New York, and Honolulu have enacted strict STR regulations that directly affect lender risk assessments. Lenders increasingly require documentation verifying STR permit eligibility before approving loans in regulated markets. A property that cannot legally operate as a short-term rental has no qualifying income.

-

Credit score thresholds. Scores below 660 typically result in denial or require compensating factors such as a larger down payment or higher DSCR. Scores between 660 and 700 may face rate adjustments of 0.25% to 0.75% compared to borrowers above 720.

-

Appraisal income premiums. Appraisers in strong STR markets sometimes assign income premiums that exceed what lenders will accept after discounting. The result is an appraisal that looks strong on paper but produces a DSCR below threshold after the lender applies its own discount methodology.

-

Documentation gaps. New STR acquisitions with no operating history rely entirely on projected income. Lenders apply greater scrutiny to projections than to verified historical income. Strong AirDNA data for comparable properties in the same market strengthens the file considerably.

“The investors who close STR loans cleanly are the ones who treat the lender’s income discount as a fixed constraint, not a negotiating point. Build your deal around discounted income from day one.”

How can investors use STR loans to scale their portfolios?

STR loans structured on DSCR give investors a scaling mechanism that conventional financing does not. DSCR-based qualification removes the personal income cap and the 10-property limit that conventional Fannie Mae guidelines impose. Each new property qualifies on its own cash flow, not on the borrower’s cumulative debt load.

Practical steps for scaling with STR financing:

-

Model every deal with discounted income. Use 70% of gross AirDNA projections as your underwriting baseline. Deals that work at 70% of projected revenue are deals worth pursuing.

-

Maintain reserves above the minimum. Lenders require 6 to 12 months of PITIA. Holding 12 months provides a buffer against seasonal downturns and regulatory changes without requiring a cash-out refinance to cover shortfalls.

-

Shop multiple lenders. STR loan terms are not standardized. Rate spreads of 0.5% to 1.0% between lenders on the same deal are common. Investor MultiFamily Capital, for example, structures STR and DSCR loans specifically for investors in New England and Florida, with underwriting focused on property cash flow rather than borrower income.

-

Use LLC ownership from the start. Structuring each acquisition in a separate LLC protects existing assets and aligns with lender requirements for business-purpose financing.

-

Prioritize markets with stable STR regulations. Properties in markets with clear, permissive STR ordinances carry lower regulatory risk, which translates to smoother underwriting and better loan terms.

Pro Tip: Review the loan approval process before submitting your first STR loan application. Investors who understand what lenders need at each stage reduce back-and-forth and close faster.

Key takeaways

STR loans qualify on property income, not personal income, making DSCR the single most critical number in every underwriting decision.

| Point | Details |

|---|---|

| DSCR drives approval and pricing | A DSCR of 1.25x or above unlocks best rate tiers; below 1.0x results in denial. |

| Income discounting is non-negotiable | Lenders reduce gross STR income by 20 to 40% before calculating DSCR. |

| Reserves are higher than conventional loans | Expect to hold 6 to 12 months of PITIA in liquid assets after closing. |

| Regulatory risk affects underwriting | Properties in STR-restrictive markets face stricter scrutiny and possible denial. |

| LLC ownership is supported | STR loans allow entity-level financing with personal guarantees, unlike conventional loans. |

What I’ve seen separate successful STR loan applicants from the rest

The investors who close STR loans cleanly share one habit: they underwrite conservatively before they ever call a lender. They pull AirDNA data, apply a 30% discount, calculate DSCR, and only proceed if the numbers work at that level. Investors who arrive with optimistic gross revenue projections and no discount applied almost always hit a wall in underwriting.

The regulatory piece is the variable that catches experienced investors off guard more than anything else. A property that cash-flows beautifully in a permissive market like Scottsdale or Gatlinburg faces a completely different lender conversation than an identical property in a city with active STR restrictions. I’ve seen deals in strong markets get denied not because of income or credit, but because the lender could not verify permit eligibility. Verify zoning and permit status before you order the appraisal.

For investors new to STR financing, the STR loan structure is worth studying in detail before your first application. For experienced investors scaling beyond five or six properties, the DSCR model is the only structure that does not create a personal income bottleneck. The math is straightforward once you internalize the lender’s discount methodology. Build your pro forma around it, and the underwriting process becomes predictable.

— Joe

Finance your next STR with Investor MultiFamily Capital

Investor MultiFamily Capital structures DSCR and STR loans specifically for real estate investors in Massachusetts, New Hampshire, Rhode Island, Connecticut, Maine, and Florida. Underwriting is based on property cash flow, not personal income, with no W-2s or tax returns required.

Closings run 10 to 21 days. LLC ownership is supported. If you are purchasing or refinancing a short-term rental property, explore DSCR loan options built for investors, or review the full DSCR loan program to compare terms. Ready to move on a deal? Submit a Deal or Apply Online to get your scenario reviewed by an investor-focused lending team.

FAQ

What is an STR loan?

An STR loan is a non-QM investment loan that qualifies borrowers based on a property’s short-term rental income rather than personal income documentation, using DSCR as the primary underwriting metric.

What credit score is needed for an STR loan?

Most STR lenders require a minimum credit score of 660 to 680, with scores above 720 qualifying for the best rate tiers and lowest down payment requirements.

How do lenders calculate income for an STR loan?

Lenders use third-party revenue data from platforms like AirDNA and appraisal rent schedules, then apply a 20 to 40% discount to gross projected income before calculating DSCR.

How long does it take to close an STR loan?

STR loan processing typically takes 10 to 21 days from application to closing, significantly faster than conventional investment loans, because no personal income verification is required.

Can I use an LLC to take out an STR loan?

Yes. STR loans support financing through LLCs and corporations with personal guarantees from principals, which is a standard structure for business-purpose investment property financing.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.