TL;DR:

- Real estate leverage involves using borrowed funds to control larger assets and increase potential returns on equity.

- Higher LTV ratios amplify both gains and risks, requiring careful stress testing of income scenarios before investing.

Real estate leverage is defined as the use of borrowed capital to control a larger property asset than your equity alone would allow, amplifying your return on equity relative to the property’s actual performance. A straightforward example: put $100,000 down on a $500,000 property, and you control a larger asset with just 20% of its value. If that property appreciates 10%, your $50,000 gain represents a 50% return on your $100,000 equity. That multiplication effect is the core mechanic every real estate investor needs to understand before deploying a single dollar of debt. Used correctly, leverage is the primary tool for building a real estate portfolio faster than cash alone permits. Used carelessly, it accelerates losses just as efficiently.

What is real estate leverage and how is it calculated?

Leverage in real estate is measured primarily through two ratios: the Loan-to-Value ratio (LTV) and the leverage ratio (LR). LTV equals the loan amount divided by the property’s appraised value. A $400,000 loan on a $500,000 property produces an LTV of 80%. Lenders use this figure to price risk, set terms, and determine insurance requirements.

The leverage ratio takes that one step further. LR equals 1 divided by (1 minus LTV). At 65% LTV, your leverage ratio is approximately 2.86x. That means equity returns vary roughly 2.86 times more than the unlevered property return. A 5% property gain becomes a 14.3% equity gain. A 5% property loss becomes a 14.3% equity loss.

The table below shows how LTV and leverage ratio interact across common financing scenarios:

| LTV | Equity Required | Leverage Ratio | Return Amplification |

|---|---|---|---|

| 60% | 40% | 2.50x | 2.5x property return |

| 70% | 30% | 3.33x | 3.3x property return |

| 75% | 25% | 4.00x | 4.0x property return |

| 80% | 20% | 5.00x | 5.0x property return |

| 95% | 5% | 20.00x | 20.0x property return |

Higher LTV does not just amplify returns. It also raises your cost of capital. Mortgage insurance requirements and higher interest rates both kick in above 80% LTV, which compresses the net return advantage you were counting on.

Pro Tip: Run your leverage ratio before you run your cash-on-cash return. If your LR is above 4x, your deal needs a significant margin of safety in rent income to survive a vacancy or rate adjustment.

What borrowing tools do investors use to apply leverage?

Real estate investment leverage is not a single product. Investors deploy several distinct instruments depending on their strategy, timeline, and existing equity position.

- Conventional and commercial mortgages are the baseline. They provide fixed or adjustable rate financing against a specific property, typically at 65% to 80% LTV for investment assets. Commercial real estate leverage typically runs 60% to 75% loan financing of purchase price, with the equity investor supplying the remaining 25% to 40%.

- DSCR loans qualify based on the property’s rental income rather than the borrower’s personal income. This makes them the preferred tool for investors building portfolios across multiple assets. Investor MultiFamily Capital structures DSCR loan products specifically for this use case.

- Bridge loans fund acquisitions or transitions where permanent financing is not yet in place. They carry shorter terms and higher rates, but give investors speed and flexibility when a deal requires fast execution.

- Fix-and-flip loans are short-term, asset-based instruments designed for value-add projects. They fund both acquisition and renovation costs, with repayment expected at sale or refinance.

- HELOCs allow investors to leverage existing equity from a property they already own as a revolving credit line to fund further acquisitions. The risk: if property values fall, your available credit shrinks and your collateral exposure grows simultaneously.

- Cash-out refinancing replaces an existing mortgage with a larger one, pulling equity out as cash. Investors use this to recycle capital into new deals without selling the original asset.

Pro Tip: A HELOC on an investment property is path-dependent. The credit available today may not be available when you need it most, because lenders can freeze or reduce lines when market values decline. Size your HELOC draws conservatively.

What is positive vs. negative leverage in real estate?

The direction leverage works in your favor depends entirely on the spread between your property’s return and your cost of debt. Positive leverage occurs when the property’s return exceeds the debt cost, which increases equity returns above what the unlevered property would produce. Negative leverage is the reverse: debt costs exceed property returns, and every dollar of borrowed money actively reduces your equity return.

Here is how the three scenarios play out in practice:

- Positive leverage. A multifamily property generates an 8% cap rate. Your debt costs 6%. The 200 basis point spread means borrowing money actually improves your equity return. The more you borrow (within reason), the better your equity yield.

- Neutral leverage. Cap rate and debt cost are equal, say both at 6.5%. Borrowing neither helps nor hurts your return on equity. The only benefit at this point is capital efficiency, freeing cash for other deals.

- Negative leverage. A property yields a 5.5% cap rate but your loan carries a 7% rate. Every dollar borrowed costs more than it earns. Your equity return falls below the unlevered property return. This scenario is common when acquisition prices are high relative to rents, or when interest rates rise after a deal is underwritten.

Negative leverage does not automatically make a deal bad. A fix-and-flip investor may accept negative leverage on a short hold if the value-add upside is large enough. But for buy-and-hold investors, negative leverage is a structural problem that compounds over time. Identify it before closing, not after.

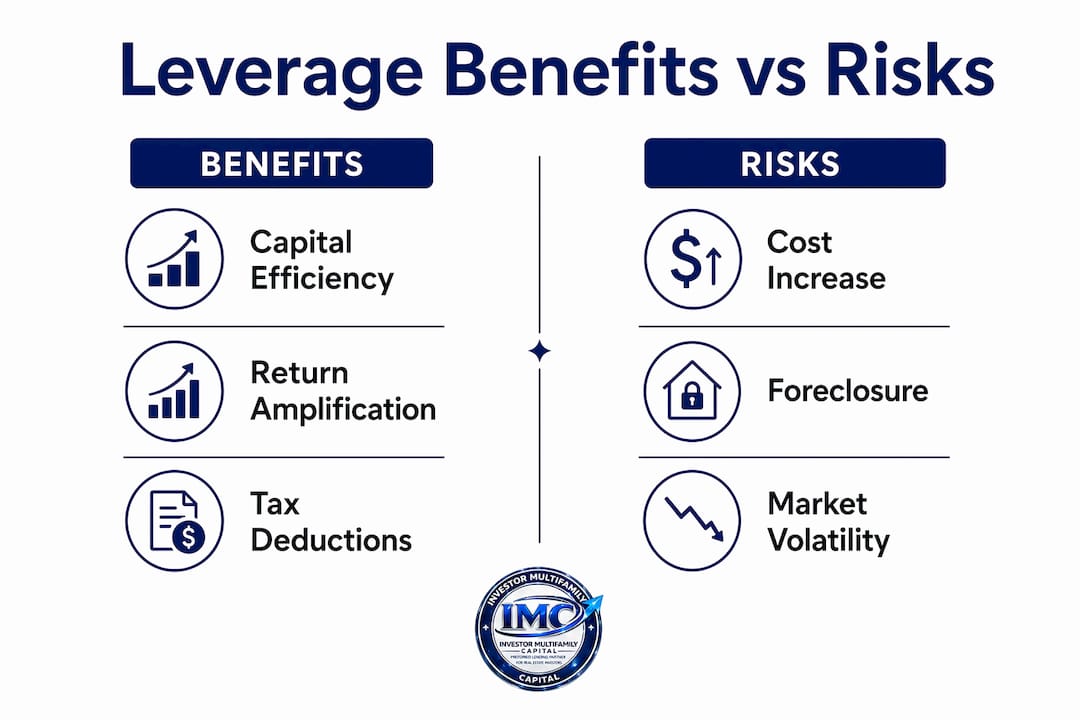

What are the main risks and benefits of real estate leverage?

Understanding leverage in real estate requires an honest accounting of both sides. The benefits are real and significant. So are the risks.

| Factor | Benefit | Risk |

|---|---|---|

| Capital efficiency | Control more property with less equity | Amplified losses if values decline |

| Portfolio growth | Acquire multiple assets faster | Increased debt service obligations |

| Tax treatment | Mortgage interest is generally deductible | Overleveraged assets face foreclosure risk |

| Return amplification | Equity returns exceed property returns | Volatility scales with leverage ratio |

| Market sensitivity | Gains accelerate in rising markets | Losses accelerate in falling markets |

The tax angle is worth noting specifically. Mortgage interest on investment properties is generally deductible against rental income, which lowers your effective cost of debt. This improves the positive leverage spread without requiring any change to the property itself.

The foreclosure risk is the scenario most investors underestimate. Higher LTV means more fragility. A property that drops 15% in value at 80% LTV leaves you with negative equity and a lender who may call the loan or refuse to refinance. Stress testing your deal at 10% to 20% value declines and 10% to 15% rent reductions before closing is not optional. It is the minimum standard for responsible underwriting.

Pro Tip: Use DSCR as your primary stress test metric. If your property’s net operating income covers debt service at 1.25x or better under a conservative rent scenario, your leverage position is defensible. Below 1.0x, you are subsidizing the property from personal cash.

How to apply real estate leverage strategy in 2026

The 2026 lending environment rewards investors who understand their numbers before approaching a lender. Rates remain elevated relative to the 2020 to 2022 cycle, which compresses positive leverage spreads and makes deal selection more critical.

Practical leverage strategy for 2026 breaks down into four execution steps:

- Target LTV ranges of 60% to 75% for buy-and-hold assets. Debt financing at these levels amplifies returns without pushing leverage ratios into fragile territory. Above 80% LTV, the cost premium and insurance requirements often eliminate the return advantage.

- Match the loan product to the hold period. DSCR loans suit long-term rental holds because they qualify on property cash flow rather than personal income. Bridge loans suit transitional assets where permanent financing follows stabilization. Fix-and-flip loans suit short holds with defined exit timelines.

- Run a real estate leverage calculator before every deal. Calculate LTV, leverage ratio, DSCR, and cash-on-cash return under base, conservative, and stress scenarios. Sophisticated underwriting combines LTV with DSCR, rental income stress tests, and debt amortization schedules. No single metric tells the full story.

- Use cash-out refinancing to recycle equity without selling. Once a property appreciates or is improved, a cash-out refinance on rental property pulls equity into your next acquisition while keeping the original asset in your portfolio. This is the core mechanic of the BRRRR strategy.

For multifamily investors specifically, the combination of DSCR underwriting and 65% to 70% LTV produces the most durable leverage position. Rental income stability at the property level becomes the primary risk variable, which is far more controllable than interest rate movements or market cycles.

Key takeaways

Real estate leverage amplifies both returns and losses in direct proportion to the leverage ratio, making disciplined LTV selection and DSCR underwriting the two non-negotiable inputs for any leveraged investment.

| Point | Details |

|---|---|

| Core definition | Leverage uses borrowed capital to control larger assets and amplify equity returns. |

| LTV drives cost and risk | Higher LTV raises interest rates, insurance costs, and portfolio fragility simultaneously. |

| Positive vs. negative leverage | Positive leverage requires property return to exceed debt cost; negative leverage destroys equity yield. |

| Loan product selection | Match DSCR loans to long-term holds, bridge loans to transitions, and fix-and-flip loans to short-term value-add plays. |

| Stress test before closing | Run DSCR and value-decline scenarios at 10% to 20% below base assumptions before committing to any leveraged deal. |

Why leverage discipline separates serious investors from the rest

I have reviewed hundreds of investor deals over the years, and the pattern is consistent: the investors who get into trouble are not the ones who used leverage. They are the ones who used leverage without stress testing it. They underwrote to best-case rent projections, accepted 85% or 90% LTV because the lender allowed it, and never asked what happens if vacancy runs at 15% for six months.

Leverage does not create value. It redistributes risk from the lender to the equity investor. When the property performs well, you capture the upside. When it underperforms, you absorb the downside at a multiple. That is the deal you are accepting every time you sign a loan document.

My practical advice for 2026: treat your leverage ratio as a fragility score, not just a return multiplier. A 3x leverage ratio on a stabilized multifamily asset with strong DSCR is a very different risk profile than a 3x leverage ratio on a single-tenant retail property with a lease expiring in 18 months. The math looks identical. The risk does not. Investors who understand loan scenarios at this level of specificity consistently outperform those who focus only on the headline return.

The 2026 rate environment has actually done serious investors a favor. It has priced out the undisciplined capital that was chasing deals at negative leverage spreads in 2021 and 2022. If you can identify assets with genuine positive leverage at today’s debt costs, you are buying into a less competitive market with better long-term fundamentals.

— Joe

Finance your next leveraged deal with Investor MultiFamily Capital

Investor MultiFamily Capital structures business-purpose financing for real estate investors across New England and Florida who are ready to put leverage to work. Whether you are acquiring a multifamily asset with a DSCR loan, executing a fix-and-flip with short-term financing, or pulling equity out of a stabilized rental to fund your next acquisition, IMC underwrites based on property cash flow, not your personal tax returns. Serving investors in MA, NH, RI, CT, ME, and FL with fast, flexible deal execution. Submit a Deal, Run Deal Analysis, or Apply Online at investormultifamily.com.

FAQ

What is real estate leverage in simple terms?

Real estate leverage means using a mortgage or other loan to buy a property with less than its full purchase price in cash, so that a smaller equity investment controls a larger asset and amplifies your return on that equity.

What is a good LTV ratio for investment properties?

Most experienced investors target 60% to 75% LTV on buy-and-hold assets. This range amplifies returns without triggering mortgage insurance requirements or pushing the leverage ratio into territory where a modest value decline creates negative equity.

What is the difference between positive and negative leverage?

Positive leverage occurs when a property’s return exceeds the cost of debt, increasing equity yield above the unlevered return. Negative leverage occurs when debt costs exceed property returns, reducing equity yield below what you would earn with no financing at all.

How does DSCR relate to real estate leverage?

DSCR measures whether a property’s net operating income covers its debt service. Lenders and investors use it alongside LTV to assess whether the leverage level on a deal is sustainable under realistic income scenarios, making it the primary stress test metric for leveraged investments.

Can a HELOC be used to leverage real estate investments?

A HELOC secured by an existing investment property provides a revolving credit line that can fund further acquisitions. The risk is that available credit shrinks if property values decline, making the strategy sensitive to market conditions at the time of drawdown.

Investor-only. Business-purpose investment property financing only. Not for owner-occupied or primary residence loans.